ecoPayz vs Skrill vs Neteller: Which E-Wallet Fits a UK Casino Player?

I get asked which of these three is “the best e-wallet” at least once a week, and I have learned to stop answering the question as asked, because it has no answer. There is no best e-wallet for UK casino play, only a best one for a particular player with a particular pattern. These three are close cousins, not rivals separated by some decisive feature, and anyone telling you one crushes the others is selling you something. The honest comparison is about fit: which wallet’s fees, speed and acceptance line up with how you actually deposit, win and cash out.

What is true is that all three sit at the top of the e-wallet pile, and the ordering is established rather than contested. Payz, the wallet formerly called ecoPayz, ranks as the third largest, behind Skrill and Neteller, which between them dominate the gambling-payments space. That ordering tells you about market share, not about which one suits you, and the gap that matters to a player is rarely the gap that shows up in a league table. Over the next few sections I will walk the real points of difference, the fees, the speed, the acceptance, the bonus quirk, and then give you the only useful framework I know: matching the wallet to the player rather than crowning a champion that does not exist.

While evaluating these popular e-wallets, players should carefully look into ecoPayz casino fees to avoid unexpected charges on their transactions.

Comparing ecoPayz, Skrill, and Neteller Features

Picture three siblings who grew up in the same house. That is roughly the relationship between these wallets. They do the same job, they look broadly alike at the cashier, and the differences between them are matters of temperament rather than function. Knowing each one’s character is more useful than memorising feature lists.

Payz is the independent of the three, operated by PSI-Pay Limited and not part of the same group as the other two. It is built around broad reach and currency flexibility, supporting more than 50 currencies including pounds, which makes it comfortable for players who move across markets or want a pound balance to avoid conversion entirely. Skrill and Neteller, by contrast, are siblings in the literal corporate sense: both are owned by Paysafe, the same parent company, which is why they so often appear together on a cashier and behave so similarly. They share infrastructure, broadly overlapping fee logic and a common heritage in gambling payments specifically, where they have been entrenched for years.

That shared ownership of Skrill and Neteller is the single most useful fact in this whole comparison, and almost nobody tells players about it. Because they sit under one parent, a casino often treats them as near-interchangeable, and crucially, a bonus exclusion or a fee policy that names one frequently names both. Payz, being independent, sometimes sits in a different bucket entirely on the same cashier. So the real first division is not three wallets ranked one to three; it is one independent wallet on one side and a pair of corporate siblings on the other. Hold that picture and the rest of the comparison falls into place.

One historical wrinkle is worth knowing because it occasionally surfaces in players’ heads as a difference that no longer exists. Skrill and Neteller were once positioned as distinct products with separate followings, and some long-standing players still keep one out of habit and treat the other as a rival. Under common ownership that distinction has largely dissolved at the level that affects you, the cashier and the terms. For a UK casino player deciding today, treating them as two doors into the same building is more accurate than treating them as competitors, and it stops you wasting effort comparing two things that a casino’s own cashier already considers a matched pair.

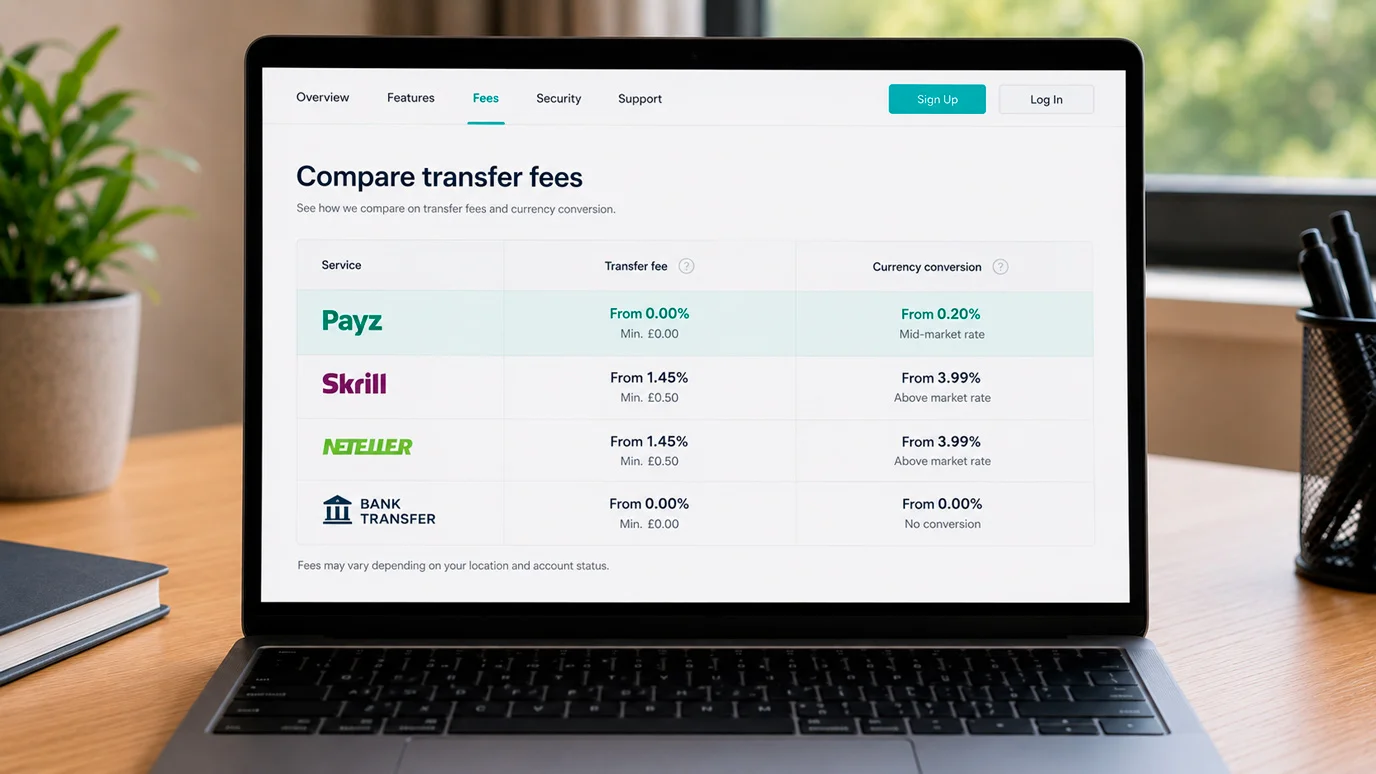

Fees, head to head

Fees are where players expect a clear winner and where they are most often disappointed, because the three wallets cost roughly the same in roughly the same situations, and the variable that actually moves your bill is not which wallet you chose but how you use it. Let me show you what I mean with Payz’s published structure, which is representative of how all three think about charging.

Payz charges a peer-to-peer transfer fee of 1.5 per cent on its Silver tier, which falls away to free once you reach Gold. Currency conversion runs at 2.99 per cent on the Classic and Silver tiers, dropping to 1.49 per cent at Gold and above. And there is a monthly inactivity charge of 1.50 euros if the account goes dormant. Now look at what that tells you. The headline fees are tiered, so your effective cost depends on your account level far more than on the brand name on the wallet. A heavy user at a high tier pays very different rates from a casual user at the base tier, even within the same wallet. Skrill and Neteller follow the same logic of tiered fees, conversion margins and dormancy charges, with the numbers in similar territory.

So the fee comparison that matters is not “which wallet is cheapest” but “where are my fees actually coming from,” and for a UK player the answer is almost always currency conversion. Consider a simple worked case. You hold euros and deposit 500 across a month at a casino billing in pounds, on a tier charging 2.99 per cent conversion. That is roughly 15 lost to the spread, on every wallet that charges a similar margin, regardless of which of the three you picked. Move to a pound balance and that 15 vanishes entirely. The lesson repeats across all three wallets: the conversion margin dwarfs the transfer fees for most casino players, and holding your money in pounds is worth more than any difference between the brands. Picking the wallet to save on fees is optimising the small number while ignoring the large one.

There is a second-order point about tiers that applies equally to all three and that frequent players should understand. The fee reductions at higher tiers are not marketing perks; they are tied to verification levels, and reaching them takes documentation and sometimes a track record of activity. For a casual player, chasing a higher tier to shave the conversion margin from 2.99 to 1.49 per cent rarely pays for the effort, because the absolute sums are small. For a high-volume player moving four or five figures a month, that halving of the margin is real money, and it is one of the few places where the choice of wallet and tier genuinely affects your bottom line. So the fee question quietly splits by player type: trivial for the casual user, who should simply hold pounds and forget it, and worth optimising for the heavy user, who should pick the wallet and tier combination that minimises conversion on their actual volume.

Speed and where each one is actually accepted

On raw speed there is nothing to choose between them, and I say that as someone who has timed more deposits and withdrawals than is healthy. All three credit deposits to a casino in seconds and receive withdrawals from a casino as fast as the casino releases them. The wallet has never been the bottleneck for any of the three; the casino’s review window is, and that is identical whichever wallet you use. So if someone tells you Skrill is “faster than Payz,” ask them faster at what, because at the rail level the claim does not hold.

Where the three genuinely diverge is acceptance, and this is the difference that should actually drive your choice. Skrill and Neteller, by virtue of their long entrenchment in gambling payments and their shared parent, are accepted at a very wide range of UK casinos, often both listed side by side. The strength of that position is not theoretical; Paysafe, the parent, reported active digital wallet users rising to 7.9 million and iGaming revenue up 28 per cent in early 2026, the kind of momentum that comes from being deeply embedded in operators’ cashiers. Payz is accepted widely too, but on any given cashier you may find one of the three present and another absent, and which is which varies by operator.

This is why I never recommend choosing a wallet in the abstract. The right wallet is partly determined by the casinos you actually intend to use, because a wallet that is not on your chosen site’s cashier is useless to you no matter how good it is everywhere else. The practical move is to check acceptance at your specific destination first, then choose among the wallets that clear that bar. Acceptance is a binary filter applied per casino, and it quietly overrides every other consideration: the cheapest, fastest wallet in the world does you no good at a casino that does not list it.

The bonus question that trips people up

Here is the trap that catches more players than fees and speed combined, and it is the one almost nobody warns you about until the bonus has already failed to apply. Many UK casinos exclude e-wallet deposits from their welcome offers, and they do it in the small print, and they often name Skrill and Neteller together because of that shared ownership.

The reasoning, from the operator’s side, is that e-wallets make it easier to move money in and out quickly, which historically made them attractive for bonus abuse, so casinos drew a line. The consequence for you is concrete: deposit with one of these wallets expecting a welcome bonus, and you may find the bonus simply does not trigger, with no error and no explanation beyond a clause you skipped. Because Skrill and Neteller are corporate siblings, an exclusion clause naming “Skrill and Neteller” is extremely common, while Payz, being independent, occasionally falls outside the same clause, though you can never assume it.

The only safe behaviour is to read the bonus terms before depositing, every time, specifically for an e-wallet exclusion. Do not assume the three wallets are treated identically, and do not assume that because a bonus accepted a card deposit it will accept your wallet. This is not a reason to avoid e-wallets, which earn their keep on privacy, speed and control. It is a reason to separate two decisions that players wrongly merge: how you want to pay, and whether you want a particular bonus. Sometimes those decisions pull in different directions, and knowing that in advance lets you choose deliberately rather than discover the conflict after the fact.

Which wallet fits which kind of player

Now the part that actually answers the question, by refusing to answer it the way it was asked. There is no winner. There is a wallet that fits your pattern, and once you know your own pattern the choice mostly makes itself.

If you play across multiple markets or currencies and value flexibility, Payz’s broad currency support and independence make it a natural fit, especially if you want a pound balance for UK play alongside other currencies elsewhere. If your priority is the widest possible acceptance at established UK casinos and you want a wallet that is almost always on the cashier, Skrill or Neteller’s deep entrenchment is the pragmatic choice, and since they are siblings, either tends to be accepted wherever the other is. If you care most about privacy from your bank statement and fast, controlled cash-outs, all three deliver that equally, so the choice drops back to acceptance and fees at your specific casino. There is real evidence that this privacy-and-speed motivation drives the whole category: in surveys of online players, around 68 per cent said they preferred e-wallets to credit cards precisely for the safety and speed they offer, which is the shared appeal that makes all three worth holding in the first place.

The framing I trust comes from inside the payments industry itself. Paysafe’s global gaming president Zak Cutler put it plainly: “Payments aren’t just a back-end function — they’re a strategic growth driver.” For an operator that means investment in the cashier; for you as a player it means the opposite reading, that the payment method is not a trivial afterthought but a real lever over your experience, your costs and your control. Choose the wallet that fits how you play, not the one that topped a list. And if you want to widen the field beyond these three, my comparison of ecoPayz versus PayPal at UK casinos covers a fourth option whose acceptance picture is very different and worth understanding before you settle.

Switching, or holding more than one

The smartest UK players I know do not pick one wallet and marry it. They hold two, and the logic is so simple it is almost embarrassing that more people do not do it. Acceptance varies by casino, bonus exclusions vary by wallet, and the occasional outage or verification hold is a fact of life. A single wallet is a single point of failure for your entire ability to play.

A sensible setup is one independent wallet and one of the corporate siblings, which between them cover almost any cashier you will meet, because where one is absent the other is usually present. Holding two costs you nothing in the base case, since you only pay fees when you transact, though you should mind the dormancy charge on any wallet you leave idle, which is exactly the kind of small, silent cost that a seasonal player forgets until it has quietly eaten a balance.

Switching between wallets, or moving money from one to another, is straightforward but not free, since transfers and conversions carry their own fees, so it is not something to do casually mid-session. The better approach is to set up both wallets properly once, keep each funded from a debit or bank source, and reach for whichever one your chosen casino actually accepts. That way the question stops being “ecoPayz or Skrill or Neteller” and becomes “which of my two wallets works here,” which is a far easier question and one you can answer at the cashier in seconds. The comparison was never meant to end in a single choice. It was meant to make you fluent in three tools that mostly do the same job, so you can pick the right one for the moment rather than the one a ranking told you to trust.

If you have made your choice, you can start playing immediately at any of the leading UK ecoPayz casinos reviewed by our experts.

The comparison questions readers send me

Prepared by the Vaultline editorial staff.