ecoPayz vs Bank Transfer at UK Casinos: Speed Against Directness

A reader once told me he had stopped using e-wallets entirely because, in his words, “why add a middleman when the bank can just send the money?” It is a clean argument and I had no quick rebuttal at the time. A bank transfer is about as direct as a payment gets — your account, the casino’s account, nothing in between.

And yet I still use the wallet for almost everything, which means the directness he prized clearly is not the only thing that matters. The two routes solve the same problem — getting money to the cashier and back — but they optimise for opposite virtues. Bank transfer optimises for directness and zero intermediaries. A wallet optimises for speed, separation and a layer of control. You cannot have both at once.

So this comes down to a single honest trade: do you want the most direct route, or the most convenient one? Below I will set out what a bank transfer genuinely does better, what the wallet does better, and how to decide which virtue your style of play actually rewards. Neither is the “right” answer in the abstract — but one of them is the right answer for you.

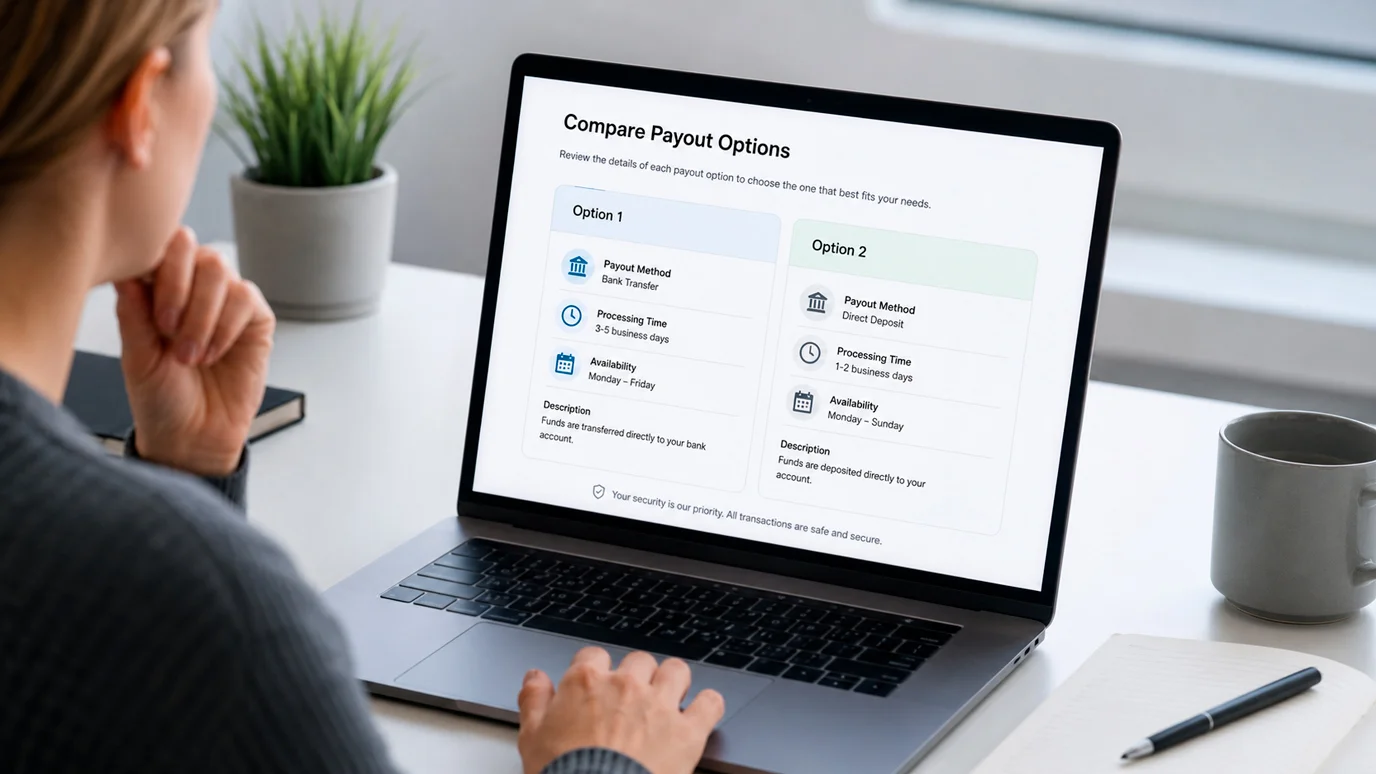

Where the Bank Transfer Genuinely Wins

Let me give the bank transfer its due, because it has real strengths the wallet crowd likes to gloss over. A transfer is the most direct payment route there is: money leaves your account and arrives at the casino with no third party holding it in between, no extra balance to maintain, no wallet tier to verify. For large, infrequent movements that directness is genuinely valuable.

It also tends to avoid the conversion margins a wallet can introduce, provided both ends are in sterling, and it sits naturally within the safer-spending framework UK regulation has been building. The credit card ban of 14 April 2020 pushed gambling firmly toward money players already hold, and a bank transfer is the purest expression of that principle — you are moving funds that exist, from an account in your own name, with your bank’s full visibility over the transaction. There is something to be said for a payment method your bank can see and vouch for in full.

The cost of all that directness is time and friction. Bank transfers can be slow, especially on withdrawals, where a payout may take days to clear rather than the near-instant arrival a wallet manages. And because the transfer links your account straight to the operator, every movement lands on your main statement under a gambling name — the same footprint issue that sends so many players looking for a buffer. Directness, it turns out, is not free.

What You Trade Up To With the Wallet

Now the other side. The reason I keep reaching for Payz despite the bank transfer’s elegant simplicity is that the wallet wins decisively on the two things I actually feel day to day: speed and separation. A wallet-funded withdrawal typically lands far faster than a bank transfer, and the wallet sits as a deliberate buffer between my account and the casino.

That buffer is the same advantage it holds over a raw bank link, and it is run on solid foundations — PSI-Pay Ltd is FCA-authorised under registration number 900011, holds customer funds in ring-fenced safeguarding accounts protected even in the event of insolvency, and has been recognised as a safe payments provider since 2008. So the “middleman” my reader objected to is not an unregulated stranger holding his cash; it is an authorised institution that keeps his money legally separated from its own. The speed comes from the wallet settling internally rather than waiting on interbank clearing, and the separation comes from the wallet, not the bank, being the thing that talks to the casino.

This is why e-wallet preference runs so high — around 68% of online players in one Paysafe study would choose a wallet over a card, and the same logic that beats the card beats the slow bank transfer too. Mobile wallets now account for a majority of global online transactions, about 53% in 2024, precisely because people will trade a sliver of directness for speed and a cleaner footprint nearly every time. The wallet’s middleman is the feature, not the bug.

Matching the Route to the Movement

The cleanest way to choose is to stop thinking about which is better overall and start thinking about the specific movement in front of you. Big and rare points one way; frequent and modest points the other, and I genuinely use both depending on the job.

For a large, one-off movement where you do not mind waiting and value the bank’s full visibility, the transfer is a perfectly rational choice — its slowness barely matters when you are not in a hurry, and its directness is a virtue at scale. For regular play where you want fast withdrawals, a clean main statement and a ring-fenced budget, the wallet is the obvious tool, and the friction of a bank transfer would only get in your way. The deciding question is frequency and urgency, not which method is “purer.”

If the wallet’s prepaid, ring-fenced character is what appeals — money set aside in advance rather than pulled live from your account — that same instinct extends to a physical card drawing on the wallet balance, which I cover in the piece on the ecoPayz prepaid Mastercard. My own habit is to keep bank transfer in reserve for the occasional large top-up and let the wallet handle the everyday rhythm of deposits and withdrawals, which captures the transfer’s directness when it counts and the wallet’s speed the rest of the time.

Prepared by the Vaultline editorial staff.